How Your CIBIL Score Can Change Your Home Loan Interest Rate

When people apply for a home loan, most of the focus usually goes toward property prices, down payment, and EMI calculations. But there is another factor that quietly plays a huge role in the background: your CIBIL score.

A strong CIBIL score can help you get lower interest rates, faster approvals, and better loan offers. A poor score, however, can increase your borrowing cost and sometimes even reduce your chances of getting a loan approved.

Since home loans usually continue for 15 to 30 years, even a small difference in interest rate can make a huge impact on the total amount you repay over time. This is why banks carefully check your credit score before approving a housing loan.

What is a CIBIL Score?

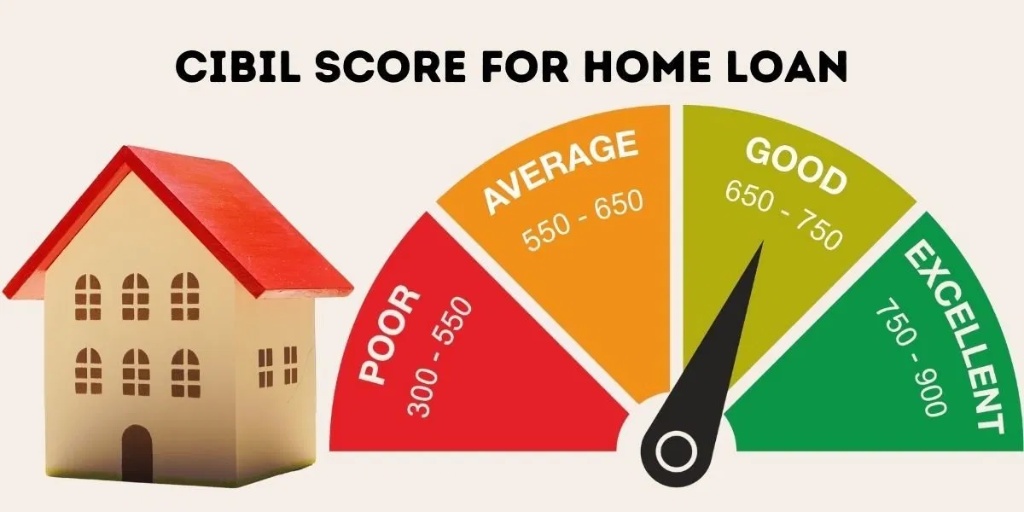

A CIBIL score is a three-digit number that represents your creditworthiness. It is issued by TransUnion CIBIL and generally ranges between 300 and 900.

This score is calculated using your financial and repayment history, including:

●Loan repayment behaviour

●Credit card bill payments

●Active loans and closed loans

●Credit utilisation ratio

●Loan and credit card enquiries

●Length of credit history

In simple words, the score helps lenders understand how responsibly you manage borrowed money.

A higher score usually indicates good financial discipline, while a lower score signals higher lending risk.

Why Is CIBIL Score Important for Home Loans?

Home loans involve large amounts and long repayment periods. Naturally, banks want to reduce the risk of defaults before lending money.

Your CIBIL score gives lenders a quick picture of your financial habits. It helps them assess:

●Whether you pay EMIs on time

●How well you manage existing debt

●Your repayment consistency

●The risk involved in approving your loan

Based on this assessment, banks decide:

●Whether your home loan should be approved

●The interest rate you qualify for

●The loan amount you are eligible for

●Repayment terms and conditions

This is one reason why two borrowers with similar salaries may still get different home loan interest rates.

How Different CIBIL Scores Affect Home Loan Interest Rates

CIBIL Score Between 750 and 900

This is considered an excellent credit score range.

Borrowers in this category are usually offered the best home loan interest rates because banks see them as low-risk customers.

Benefits may include:

●Lower EMIs

●Faster loan approvals

●Better loan offers

●Higher eligibility amounts

●Better negotiating power with lenders

Many borrowers with strong scores also experience smoother processing during loan approval.

CIBIL Score Between 700 and 749

This range is generally considered good by most lenders.

Borrowers still have high chances of approval, although the interest rate may be slightly higher than what top-tier borrowers receive.

In most cases, banks offer:

●Competitive interest rates

●Standard repayment terms

●Easier documentation process

Even a small improvement in this score range can sometimes help borrowers secure better loan terms.

CIBIL Score Between 650 and 699

This range falls into the average category.

Home loan approval is still possible, but lenders may become more cautious while evaluating income, job stability, and existing financial commitments.

Borrowers may experience:

●Slightly higher interest rates

●Increased EMI burden

●Lower approved loan amount

●Additional verification checks

This category is often treated as medium risk by lenders.

CIBIL Score Between 550 and 649

This is considered a weaker credit profile.

Banks may still approve loans in some cases, but borrowers often face stricter conditions and higher borrowing costs.

Common challenges include:

●Higher home loan interest rates

●Lower loan eligibility

●Requirement for a co-applicant

●Additional income proof and documentation

For many borrowers, improving the credit score before applying can lead to much better loan offers.

CIBIL Score Below 550

A very low CIBIL score can significantly reduce your chances of getting a home loan approved.

Lenders may consider the borrower high risk because of poor repayment history or excessive debt.

Even if approval happens, borrowers may face:

●Very high interest rates

●Limited lender options

●Shorter repayment periods

●Strict loan conditions

In such situations, improving credit health before reapplying is usually the smarter financial decision.

Why Even a Small Interest Rate Difference Matters

Many people underestimate how much a small interest rate difference can affect long-term repayment costs.

For example, consider a Rs 50 lakh home loan for 20 years:

●At 8.5% interest, the total interest paid may be around Rs 54 lakh

●At 9.5% interest, the total interest paid may increase to around Rs 63 lakh

That is nearly Rs 9 lakh in additional interest, mainly because of differences in credit profile and loan pricing.

This is why maintaining a healthy CIBIL score can save borrowers a significant amount over the life of a loan.

Other Ways Your CIBIL Score Affects Home Loans

Apart from interest rates, your credit score may also influence:

●Loan processing speed

●Processing fees

●Prepayment flexibility

●Approval timelines

●Requirement for guarantors or co-applicants

Borrowers with stronger credit profiles generally receive more flexible and favourable loan terms.

How to Improve Your CIBIL Score Before Applying

Improving a credit score takes consistency and disciplined financial habits.

Some practical ways to improve your score include:

●Paying EMIs and credit card bills on time

●Keeping credit card usage below 30% of the limit

●Avoiding multiple loan applications within a short period

●Maintaining a healthy credit mix

●Regularly checking your credit report for errors

Many financial experts recommend improving your score at least six months before applying for a home loan.

Final Thoughts

Your CIBIL score is more than just a number on a credit report. It directly affects your home loan eligibility, interest rate, EMI amount, and overall borrowing cost.

A higher credit score can help you secure better loan offers and save lakhs of rupees over the years. For anyone planning to buy a home, maintaining good credit discipline is one of the smartest financial decisions you can make.

Frequently Asked Questions

What is considered a good CIBIL score for a home loan?

A CIBIL score of 750 or above is generally considered ideal for getting lower home loan interest rates.

Can I get a home loan with a low CIBIL score?

Yes, but approval may become difficult and lenders may charge higher interest rates depending on your financial profile.

Does salary matter more than CIBIL score?

Both are important. A higher salary improves repayment capacity, but lenders still consider the CIBIL score a major approval factor.

How long does it take to improve a low credit score?

In many cases, disciplined repayment habits and proper credit management can improve scores within 6 to 12 months.

Does checking my own CIBIL score reduce it?

No. Checking your own score is considered a soft enquiry and does not affect your credit score.

Do all banks follow the same CIBIL score criteria?

Most lenders use the same CIBIL report, but approval policies and interest rates may vary from one bank to another.